Every year we conduct surveys on important anti-money laundering (AML) topics. A recent survey focused on the topic of Marijuana Related Businesses (MRBs). While marijuana remains illegal on the federal level, more states have begun legalizing both adult and recreational marijuana on a state level. Although the political landscape has changed, with the Democrats controlling the White House and Congress, it is still uncertain whether or not both the House and Senate will agree on a bill to legalize marijuana federally; or at least pave the way for the financial institutions to bank them without fear of fines or penalties. The House recently passed the Safe Banking Act, that would allow financial institutions to bank marijuana without fear of any regulatory penalties for just banking it. So, all eyes are on Washington to see what will happen in the months ahead.

Every year we conduct surveys on important anti-money laundering (AML) topics. A recent survey focused on the topic of Marijuana Related Businesses (MRBs). While marijuana remains illegal on the federal level, more states have begun legalizing both adult and recreational marijuana on a state level. Although the political landscape has changed, with the Democrats controlling the White House and Congress, it is still uncertain whether or not both the House and Senate will agree on a bill to legalize marijuana federally; or at least pave the way for the financial institutions to bank them without fear of fines or penalties. The House recently passed the Safe Banking Act, that would allow financial institutions to bank marijuana without fear of any regulatory penalties for just banking it. So, all eyes are on Washington to see what will happen in the months ahead.

The number one concern when it comes to banking MRBs, since banking any cash intensive business or any type of high-risk entity, is risk. The goal of our survey was to gain a better understanding of how the financial industry is addressing MRBs and how financial institutions are assessing and mitigating the risks that come with this risk.

As we conducted our survey, the majority of our participants were BSA and Compliance Officers. Since the regulators have not defined exactly what is an MRB, it is the responsibility of the Senior Management and Board of Directors to define what they consider to be an MRB. Some institutions use a two-tier approach in which a business works directly with marijuana or it does not. Other institutions consider an MRB to be a business with 50% or more of their revenue derived from marijuana businesses, while any business with less than 50% derived from marijuana is not an MRB.

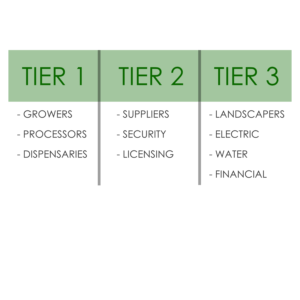

For the purpose of our survey, we used a three-tier approach. Institutions that use a three-tier approach, usually define them as followed: Tier 1 is classified as “seed-to-sale” and consists of businesses who directly handle the plant such as growers, processors, or dispensaries. Tier 2 are MRBs that have no direct contact with marijuana but primarily service Tier 1 companies that do. Tier 2 companies include suppliers, security firms, licensing consultants, etc. Tier 3 MRBs are those who provide products and services to Tier 1 or 2 MRBs, but the majority of their business is not marijuana related. Tier 3 would include landscapers, the electric company, water company, financial services, etc.

For the purpose of our survey, we used a three-tier approach. Institutions that use a three-tier approach, usually define them as followed: Tier 1 is classified as “seed-to-sale” and consists of businesses who directly handle the plant such as growers, processors, or dispensaries. Tier 2 are MRBs that have no direct contact with marijuana but primarily service Tier 1 companies that do. Tier 2 companies include suppliers, security firms, licensing consultants, etc. Tier 3 MRBs are those who provide products and services to Tier 1 or 2 MRBs, but the majority of their business is not marijuana related. Tier 3 would include landscapers, the electric company, water company, financial services, etc.

Whatever definition your institution uses, it is important to articulate that definition in your policy. Your procedures should be designed to mitigate the risks of the MRB definition you use. Once you have defined your MRBs, be sure to train your staff to ensure they have a clear understanding of your definition to enable them to accurately identify MRBs from account opening and throughout the span of the client relationship. According to our survey, most participants, 65%, indicated their institution has a policy stating they are not banking Tier 1 MRBs. Only 5% of our survey participants indicated their bank’s policy allows banking Tier 1 MRBs and 23% of participants’ bank’s policy allows them to bank both Tier 1 and Tier 2. On the other hand, almost one-third of the institutions surveyed are banking Tier 1 MRBs.

We compared the results to our First Banking MRBs Survey in 2018 and similarly, only 3% of participants had reported banking only Tier 1 MRBs and 45% reported banking only Tier 2 MRBs. We found more participants in 2018 (9%) who reported banking both Tier 1 and Tier 2 MRBs compared to only 5% in 2021. It is interesting to note that as more states legalize both recreational and medicinal marijuana, it is less common to bank multiple tiers of MRBs.

We asked our participants if their institution has had a state or a federal exam since they began banking MRBs and if so, what was the feedback they received from the regulators. Almost half of our participants’ financial institutions have had a state or federal exam since banking MRBs. Of those participants, 53% did not receive any feedback from examiners and 42% received favorable feedback. Only 5% of our participants received feedback where they needed to improve their program. Since most institutions are concerned that marijuana is illegal on the federal level, it is interesting that the regulators would appear less concerned that financial institutions are banking it as long as they have a robust BSA/AML program to manage the risks.

FinCEN requires the filing of three different types of Marijuana-related Suspicious Activity Reports (SARs):

FinCEN requires the filing of three different types of Marijuana-related Suspicious Activity Reports (SARs):

- Marijuana Limited SARs – no reason to believe the marijuana-related business is violating state law or raising any red flags.

- Marijuana Priority SARs – Suspicion that the marijuana-related business is violating state law and raises red flags.

- Marijuana Termination SARs – termination of a marijuana-related business account.

Based on our survey, 84% of institutions have not filed any marijuana related SARs and 72% have not even filed a marijuana terminated SAR for an existing MRBs relationship. Only 16% of our participants filed between 1-5 Marijuana Priority SARs. So even though the marijuana industry raises many concerns with bankers, it appears that the majority of marijuana-related businesses are working within federal guidelines and are seeking a strong partnership with the financial institutions in the area of compliance and mitigation of risk.

Our participants were asked to indicate what their institution believes is the greatest risk of banking MRBs. Regulatory risks were indicated by 42% of participants, which is interesting because that is the risk most people think of first. However, KYC/ Due Diligence risk was reported by 30% of participants, Transaction Monitoring risks and Legal Issue risks were identified by 28% each, and 16% reported cash management as one of their institution’s greatest risks. This shows that even if marijuana is legalized on the federal level, MRBs will still be a high-risk business and will require a lot of extra effort to manage the risk.

In 2018, we also asked survey participants to indicate what their institution believes to be the greatest risk of banking MRBs. In our 2018 survey legal issues were believed to be the greatest risk reported by 56% of participants. Even though the federal status of marijuana has not changed since 2018, we can see that as more states legalize marijuana, the legal risks are not the only concern to financial institutions. In fact, legal issues weren’t even among the top three risks three years later.

Our survey asked participants if their institution will continue to support MRBs in the future. Comparing the results to our 2018 survey, we did see more banks showing an interest in banking MRBs, but only by a 16% increase. For those that reported their institution will not support MRBs, their most common reason was the legal concerns between the state and federal government.

For those institutions that state in their policy they are not banking MRBs, it is vital they are taking the proper steps to ensure they are following their own policy. Our survey asked institutions to identify how they are verifying their institution does not bank MRBs. The two main ways reported by 83% of participants were conducting in-house research and having additional KYC measures in place to identify MRBs. Only 17% of our participants reported using a data service list.

The results were similar to our 2018 survey where the majority of participants used in-house research to ensure their institution is following their own policy in not banking MRBs. The next two common responses by 17% of participants each were conducting Credit/Background Checks and using Additional KYC measures to ensure their policy was being followed. It is important to implement proper procedures and processes to ensure you are not banking MRBs if that is what your policy states.

We also asked participants who do not currently bank MRBs what their greatest concern as to why their institution is not banking them. The number one concern of 66% of our participants is that marijuana is illegal on the federal level and/or because marijuana is illegal in their state. These financial institutions are concerned about the regulatory and legal pressures that come with banking MRBs because of the legality issues around marijuana. This survey revealed that regulators are cracking down on banks because of their BSA programs, not because they are banking MRBs.

For those who do bank MRBs, our survey sought to identify the greatest challenges these institutions face. The number one challenge reported by 28% of our participants was transaction monitoring. When you present your MRB program to your Board and Senior Management, this is a key piece to address. It will greatly affect your Return on Investment (ROI) if you need to increase staff and implement additional monitoring. Cash Management was also reported by 14% of participants as being the most challenging. Remember, since MRBs are often cash businesses, they will always be a high risk even if marijuana becomes legal or other laws are passed to assist financial institutions in banking them.

Before your institution determines if they will or will not bank MRBs, it is critical to determine if MRBs fit into the business plan and strategic goals of your financial institution. If you determine MRBs are not what you want to bank, it is important to delineate that in your policy and ensure that you aren’t truly banking them by implementing effective procedures and processes. If you do choose to bank them, remember our survey concluded that regulators and examiners are focusing on the quality of your bank’s programs, not the fact that your institution is banking MRBs. So, begin by diving into the industry and educating yourself on the MRBs you want to bank. Understand their business model, how they conduct business, and process transactions. Then develop a risk assessment to cover all the types of risks associated with banking the types you plan to service. Once you complete your risk assessment, determine what policies, procedures, and software (if any) you need to cover those risks. Do a staffing analysis and consider your ROI to determine the volume of MRBs you want to bank. Before banking your first MRB, present your program plan to your regulators so you know if any area of your plan presents concerns to them. Then start slowly with one or two MRBs to build a strong foundation and program around these entities. Remember, marijuana can be a profitable line of business for your institution, but it can also cost you a ton of money if you do not manage the risks properly!